It may not sound familiar to you, but chances are if you’ve applied for public aid, the IPREM (Spanish National Income Tax) has been one of the key factors in obtaining it. Let’s take a closer look at this little-known value to learn how it works and, above all, how it impacts our daily lives.

Having a good financial education is vital to successfully navigate many aspects of life, not just the financial one. This is the case with the IPREM ( Income and Earn Income Tax Index), which is used in various benefits and public aid offered by the State, including housing and education. This is a relatively new index, having come into effect in 2004 , but since then, it has been gaining ground in determining more and more aid options. If you haven’t heard of it yet, there’s no better time than now:

What is the IPREM

The acronym IPREM stands for Public Indicator of Multiple Effects Income . It is a theoretical value used to determine the income threshold for an individual or family when it comes to obtaining a benefit or social assistance.

Before the IPREM (i.e., from 2003 onward), this work was carried out by the Interprofessional Minimum Wage ( SMI ), which allowed us to determine whether a person’s income was above or below a certain threshold. However, although everything was clearer with the SMI, it didn’t take into account the possibility of receiving other benefits or income. To try to address this discrepancy and achieve a more equitable and fair distribution of benefits, the IPREM was created.

How the Multiple Effects Public Income Indicator Works

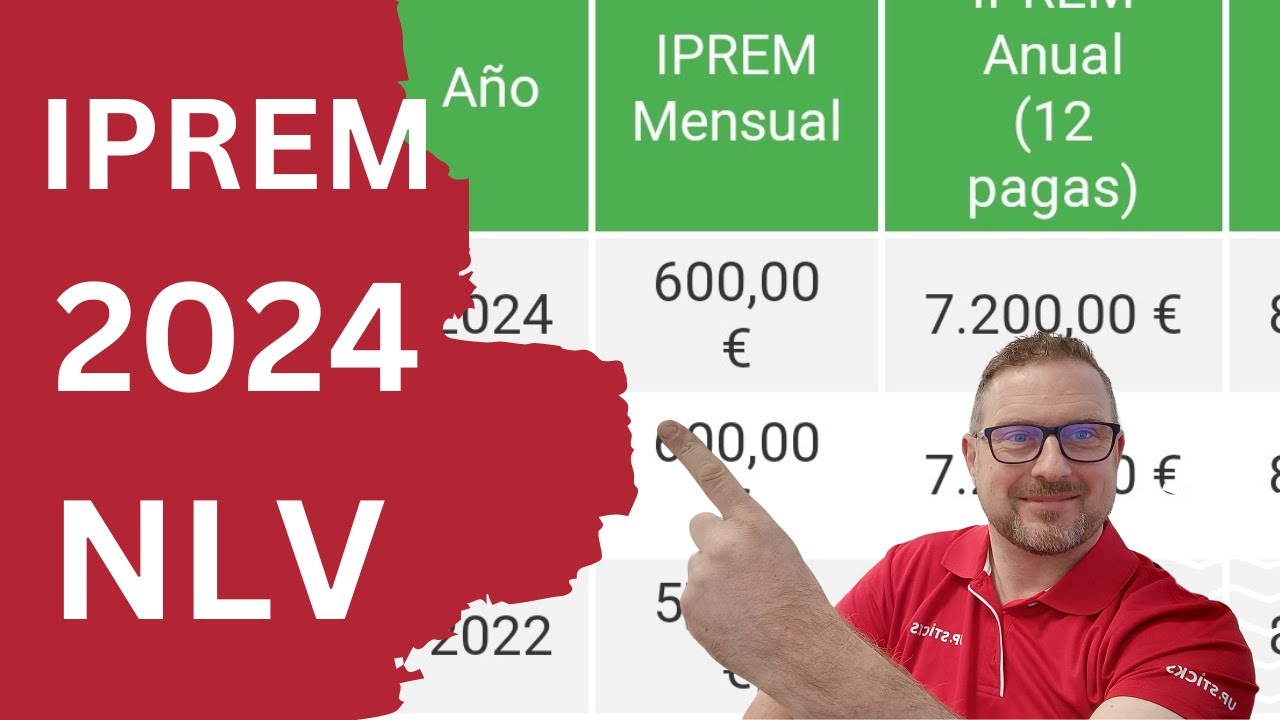

To find out the value of this economic indicator, you don’t need a calculator. Its value is set each year by the Council of Ministers when preparing the General State Budget, which is usually done at the beginning of the last quarter of the year. The annual value of the IPREM is also published in the Budget Law for easy reference.

Just because it’s decided every year, however, doesn’t necessarily mean it changes . This year, for example, the increase was planned but remained at the same level as in 2024 and 2023, at €600 per month , which means an annual total of €7,200 if there are 12 payments or €8,400 if there are 14. These figures, however, haven’t always been these. Let’s see how this economic indicator has evolved.

The evolution of the IPREM over the years

As we can see, this economic indicator has increased by approximately 30% in just over two decades . Is it a good thing that it isn’t updated every year? A priori, this makes the conditions for accessing certain aid more restrictive for those individuals or families who have seen their income increase due to salary increases. While this is the theory, in practice we see that this is not uncommon. In fact, between 2010 and 2020 it was updated only once , so it’s possible that the current value will remain the same for another year.

The different contexts where it is used

As we have been saying, this indicator is used as a reference threshold for different types of benefits linked to very different areas, such as employment or housing.

To be more specific, the IPREM comes into play when it comes to accessing:

- Protected Public Housing (VPO), both purchase and rental

- Youth rental bonus

- Scholarships and grants for study and training (from primary school to university or vocational training)

- Electricity and thermal social bonus

- Residence applications from foreigners

- Personal Income Tax bonus for large families

- Free legal assistance

The IPREM is also key when calculating things like:

- Minimum and maximum amounts of contributory unemployment benefits

- Amounts of other unemployment benefits such as the subsidy for those over 52 years of age

- Severance pay

- Amount of the Minimum Vital Income (IMV)

Learning to handle the IPREM with ease

When you read the documentation for a grant, you’ll likely find the IPREM in a phrase like this: «The benefit will be 80% of the IPREM plus one-sixth .» As we can see, many grants will require a level below the IPREM , but with a very specific threshold.

In numbers:

Limit: 80% of the IPREM

IPREM = €600

600*0,8 = 480 €

Other times, however, they multiply their value , as happens when calculating the maximum unemployment benefit limits for a person with children, where the limit is set at 200% of the IPREM plus one-sixth (1,200 + 200).

In this way, we see that the IPREM, despite being a specific reference value, can be applied and take one form or another depending on the benefit or aid, something that is done to allow or restrict access to it.

Net or gross?

This is a noteworthy question. Contrary to what one might think, when comparing income with this economic indicator, we should compare it with gross income (i.e., before taxes and withholdings), rather than net income. It’s true that what we receive is the latter, but taxes are our responsibility and, therefore, are part of our income… even though we often don’t see them.

In the case of family units, all family incomes are added together . This explains why an excellent way to increase the IPREM limits is through the number of children , since the more children there are, the higher the coefficient and, therefore, the greater the chances of receiving aid.

“Children generally apply as a corrective percentage, increasing the maximum income limit allowed by the IPREM.”

Wait a minute… economic indicator?

We’ve been saying several times that the IPREM is an economic indicator, but what is an economic indicator? It’s a piece of data , usually monetary, whose value isn’t real, but rather theoretical, or rather, statistical . They are used to analyze the state of the economy and make comparisons with past data or other realities, which, among other things, allows us to draw conclusions or make predictions for the future.

There are economic indicators to analyze key factors such as employment, inflation, and growth, among others. Some of the most famous are:

- The Unemployment Rate

- GDP (Gross Domestic Product

- The CPI (Consumer Price Index)

- The Interest Rate (TIN)

- The Balance of Payments

- Public Debt

- The Public Deficit

- The Risk Premium

- Consumer Confidence

- Etc.

Continue improving your financial literacy

As you can see, even getting financial aid requires some math and a little knowledge that, unfortunately, they didn’t teach us in school. But good fortune is never too late. That’s why at ViveMasVidas, you have all kinds of free content to improve your financial education : tips for saving better, information for investing wisely, how to prepare for your retirement, tricks for traveling on a budget, and much, much more. And if you prefer, we can send you only what interests you by email. Will you sign up for our newsletter?